Buying an investment property under a trust can offer meaningful advantages—such as asset protection, estate planning efficiency, and tax management—but it also introduces legal complexity, ongoing costs, and compliance obligations that do not suit every investor. Whether a trust structure is appropriate depends on your investment horizon, income profile, family circumstances, and jurisdiction-specific trust law.

What Does It Mean to Buy an Investment Property Under a Trust?

Buying an investment property under a trust means the legal owner of the property is a trust—not an individual—while one or more beneficiaries receive the financial benefits. A trustee (either an individual or a corporate trustee) holds and manages the property on behalf of those beneficiaries according to the trust deed.

In practical terms, rental income, capital gains, and expenses flow through the trust structure rather than sitting directly on an individual’s balance sheet. This separation between legal ownership and beneficial ownership is the defining feature of trust-based property investment.

Trusts are commonly used for long-term investment properties rather than short-term flips because the structure is designed for control, continuity, and risk management—not speed or simplicity.

Why Do Investors Buy Investment Property Under a Trust?

Investors typically use trusts to protect assets, manage tax exposure, and plan for intergenerational wealth transfer. The appeal is strategic rather than speculative.

One primary reason is asset protection. When structured correctly, a trust can help shield investment property from personal liabilities, such as business risks or creditor claims, because the property is not owned in an individual’s personal name.

Another driver is income distribution flexibility. Certain trusts allow income to be allocated among beneficiaries in a way that aligns with their tax positions, subject to local tax law. This can smooth income over time or across family members, though it must be done within strict legal boundaries.

Trusts are also widely used in estate planning. Because the trust continues to exist even if a beneficiary or trustee dies, investment property held in trust can pass to the next generation without triggering the same probate delays associated with personally held real estate.

Common Trust Structures Used for Property Investment

Not all trusts function the same way. The advantages and limitations of buying investment property under a trust depend heavily on the specific trust type used.

Discretionary trusts (often called family trusts) give the trustee discretion over how income and capital are distributed among beneficiaries. These are commonly used by family investors who want flexibility and control, but they come with tighter lending conditions and stricter compliance.

Fixed or unit trusts allocate income and capital according to predefined units, similar to shares. These are often preferred for joint ventures or unrelated investors because entitlements are clearly defined, reducing disputes but also limiting flexibility.

Hybrid trusts combine elements of discretionary and fixed trusts, though their use has declined in many jurisdictions due to regulatory scrutiny and changing tax interpretations.

Choosing the wrong trust type can undermine the intended benefits, which is why trust-based property investment is rarely suitable without legal and tax advice tailored to the investor’s jurisdiction and objectives.

Understanding the mechanics and motivations behind trust ownership is essential before weighing the advantages and disadvantages. The next stage is to assess where trusts deliver genuine benefits—and where they introduce risk, cost, or constraint.

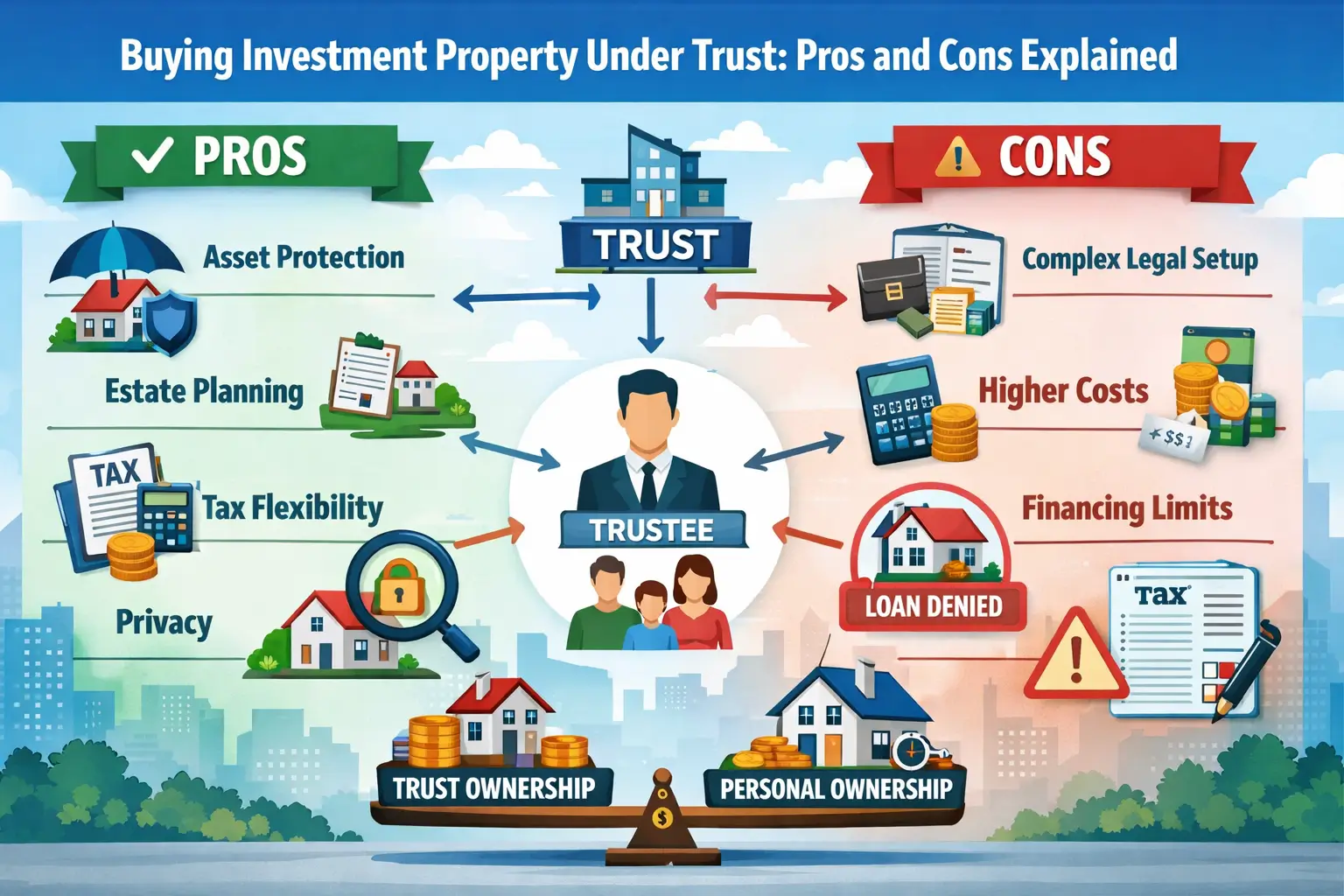

Pros of Buying Investment Property Under a Trust

Buying investment property under a trust can deliver structural advantages that are difficult to replicate through personal ownership, particularly for long-term investors managing risk, succession, and income distribution.

Asset protection: A properly established trust can separate personal risk from property ownership. If an investor faces business failure, litigation, or creditor action, trust-held property may be better insulated because it is not owned in the individual’s personal capacity. This protection depends on correct setup, timing, and ongoing compliance.

Estate planning continuity: Trusts do not cease to exist when an individual dies. This allows investment property to pass to future beneficiaries without triggering probate-related delays, forced sales, or fragmented ownership. Control can remain with a chosen trustee, preserving investment strategy across generations.

Income distribution control: Certain trust structures allow income to be distributed among beneficiaries in a controlled manner. This can be useful where household income fluctuates or where beneficiaries have differing tax thresholds. Distributions must always follow trust law and tax rules; flexibility is not unlimited.

Privacy benefits: In many jurisdictions, trust ownership offers a degree of privacy compared to personal ownership. Property title records may list the trust or trustee rather than revealing individual beneficiaries, which some investors value for discretion.

Cons and Limitations of Buying Property Under a Trust

Trust ownership introduces complexity and cost that can outweigh its benefits for smaller portfolios or short-term strategies.

Higher setup and ongoing costs: Establishing a trust involves legal documentation, professional advice, and registration requirements. Ongoing costs typically include accounting, compliance filings, trustee administration, and periodic legal reviews. These costs persist regardless of property performance.

Financing constraints: Lenders generally view trusts as higher-risk borrowers. Loan-to- value ratios are often lower, interest rates may be higher, and personal guarantees from trustees or beneficiaries are frequently required. This can reduce borrowing capacity compared to individual ownership.

Reduced access to tax concessions: In many jurisdictions, trusts do not qualify for certain capital gains discounts, first-time buyer incentives, or personal tax allowances. Investors expecting these benefits may find trust ownership financially inefficient.

Irreversibility: Once property is acquired under a trust, transferring it out can trigger stamp duty, capital gains tax, or other transfer costs. A poorly chosen structure is difficult and expensive to unwind.

Trust Ownership vs Personal Ownership: What Actually Changes?

The decision to buy investment property under a trust fundamentally alters how risk, income, and control are managed—not just how tax is calculated.

Under personal ownership, the investor has direct control, simpler financing, and straightforward tax reporting. However, personal assets and investment assets are legally intertwined, increasing exposure to personal liability and estate disruption.

Trust ownership priorities structure over simplicity. Control is exercised through trustee decisions, income flows through defined rules, and compliance obligations are higher. In return, investors gain continuity, potential asset protection, and strategic flexibility that supports long-term planning.

For first-time investors or those purchasing a single rental property, personal ownership often remains the more practical option. Trusts tend to become relevant once portfolios grow, family involvement increases, or risk exposure becomes material.

Understanding the advantages and limitations is only part of the decision. The next step is examining costs, legal obligations, tax treatment, and common mistakes that determine whether a trust structure genuinely works in practice.

Legal and Tax Considerations When Buying Property Under a Trust

Buying an investment property under a trust carries legal and tax consequences that differ materially from personal ownership. These consequences are governed by local trust law, property law, and tax regulations, which vary by jurisdiction.

From a legal perspective, the trust deed is the controlling document. It defines who can benefit from the property, how income and capital may be distributed, and the powers and limitations of the trustee. A poorly drafted deed can restrict refinancing, limit income flexibility, or invalidate asset protection objectives.

Tax treatment is equally critical. Rental income is typically taxed at the trust or beneficiary level, depending on whether income is retained or distributed. Capital gains treatment may differ from individual ownership, and some jurisdictions impose higher effective tax rates on undistributed trust income.

Compliance obligations are ongoing. Annual filings, accurate distribution records, trustee resolutions, and proper accounting are essential. Failure to meet these requirements can result in penalties or loss of intended tax outcomes.

Common Mistakes Investors Make With Trust-Owned Property

Trust structures fail most often due to misuse rather than inherent flaws. The following mistakes repeatedly undermine trust-based property strategies.

Setting up a trust after signing contracts: Asset protection benefits generally do not apply if a trust is created after liabilities arise. Timing matters.

Using trusts for short-term or low-value investments: The fixed costs of trust administration can outweigh benefits when rental income or capital growth is modest.

Ignoring lender requirements: Many investors assume financing rules are identical to personal borrowing. In reality, trust loans often require additional guarantees and documentation.

Self-managing without professional oversight: Trusts are legal structures, not casual arrangements. Poor record-keeping and informal distributions can invalidate tax positions.

Who Should—and Should Not—Buy Investment Property Under a Trust

Trust ownership is best suited to investors with long-term horizons, growing portfolios, business exposure, or clear succession planning needs. It is commonly used by families managing shared assets, entrepreneurs separating business and personal risk, and investors planning multigenerational wealth transfer.

Conversely, trusts are often unsuitable for first-time buyers purchasing a single rental property, investors prioritizing maximum borrowing capacity, or those seeking simplicity and minimal administration. In these cases, personal ownership frequently delivers better net outcomes.

The determining factor is not tax minimization alone, but whether the trust structure aligns with the investor’s risk profile, investment scale, and time horizon.

Frequently Asked Questions

Is it legal to buy an investment property under a trust?

Yes. Trusts are widely used legal structures for property ownership, provided they comply with local

trust, property, and tax laws.

Can a trust get a mortgage for an investment property?

Yes, but lending criteria are usually stricter. Lenders often require personal guarantees and may offer

lower loan-to-value ratios.

Does buying property under a trust reduce tax?

Not automatically. Trusts provide income management flexibility, but tax outcomes depend on structure,

distributions, and jurisdiction.

Can I live in a property owned by my trust?

This depends on the trust deed and local tax law. Occupying a trust-owned property may trigger tax or

compliance issues.

Is a trust better than personal ownership for landlords?

It can be for landlords with multiple properties, higher risk exposure, or estate planning goals.

Simpler portfolios often benefit more from personal ownership.

Key Takeaways

- Structural choice matters: Trust ownership changes how risk, income, and control are managed.

- Benefits are strategic: Asset protection and succession planning—not simplicity— drive trust use.

- Costs and compliance are ongoing: Trusts require continuous administration and professional oversight.

- Not for every investor: Trusts suit long-term, higher-complexity investment strategies.

References

- General principles of trust law and property ownership

- Residential property taxation frameworks (jurisdiction-dependent)

- Standard lending practices for trust borrowers